The Resource Blog

|

|

|

No one wants to think that at some point in their life they're going to need someone to take care of them. We all like to think we'll be healthy, strong and capable for years and years to come. At some point we have to face the fact that we're going to get old and with that may come challenges. Discussing Long-term Care insurance with your younger clients is something to consider doing now. And we have a way to open the door to this conversation without them shutting it down.

70% of Americans over age 65 will need some sort of Long-term Care.

Ask your client to think about their parents and/or grandparents and their health. Ask them if they have family members who are utilizing Long-term Care services (Home Health Aide, Nursing Home, Assisted Living Facility); it will help make an impact on their decision to consider purchasing Long-term Care insurance.

If they give you the argument that their parents/grandparents are healthy and longevity runs in their family, you can acknowledge that, but then you can also point out the facts below if the statistic above doesn't nudge them:

If you need help with Long-term Care products or just have questions, please reach out to us. And if you're new to selling Long-term Care insurance, request our Getting Started with Long-term Care guide.

You're entering the world of Medicare solutions and you now have to select an FMO to work with, but how do you choose? When you Google 'Medicare FMOs' there's a long list and many are even sponsored. When it comes right down to it, FMOs are essentially the liaison between you and the insurance carriers you contract with. You have to go through an FMO in order to represent multiple carriers to your clients. If you don't, you'll have to look into becoming captive with an insurance company which will only allow you to sell their specific products. So back to your FMO research. Ultimately you need to find a partner who will be there to work with you to help you grow. Some important things to consider before placing all your contracts with one FMO are: longevity in the industry, selection of carriers and products, commission structure, education and training, marketing and sales support, quoting and enrollment tools, lead generation and finally back office support.

Below are some questions you should get answers to before placing your contracts with any FMO:

When you partner with an FMO that wants you to succeed, you're headed on a path for success. Do your research and be sure you get a good feeling about the organization before committing. The right FMO will fuel you with all the tools and resources you need to have a rewarding and profitable career.

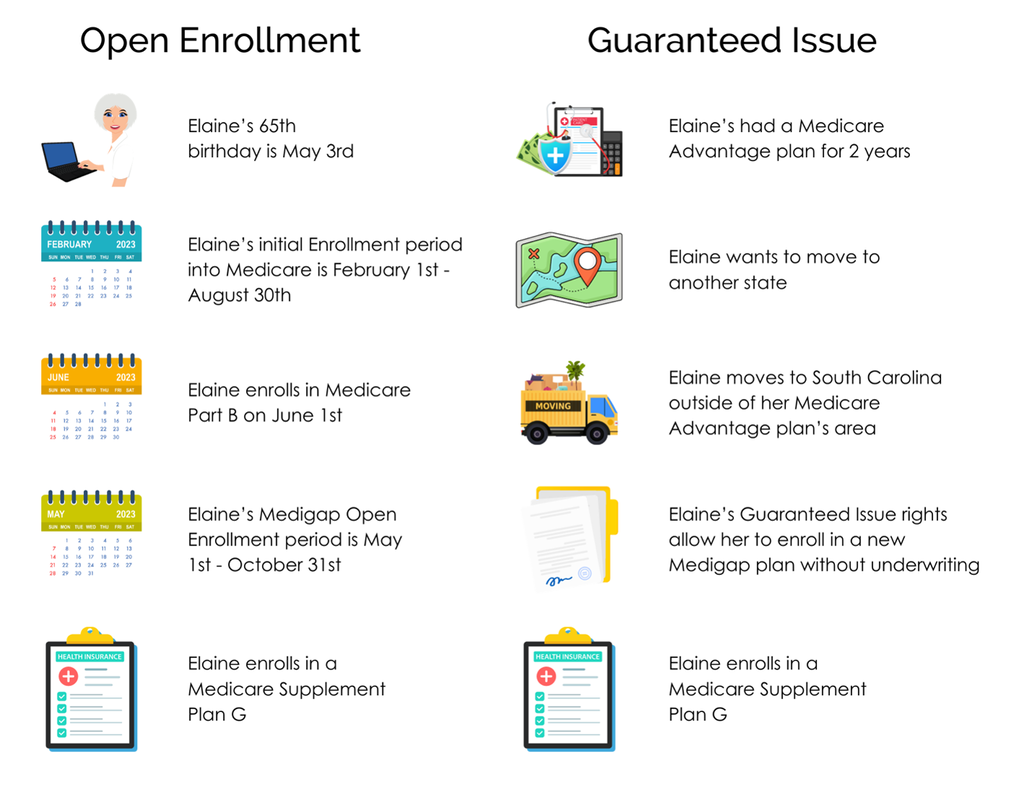

When it comes to Medicare Supplement policies there are times and situations when your client has the right to enroll in a Medigap plan without answering any health questions. The most important of those times being during their six month Medigap Open Enrollment period. This occurs when your client turns 65 or when they first enroll in Medicare Part B.

However, there may be times when you have a client who wants to enroll in a Medicare Supplement and they fall outside of their Open Enrollment period. Perhaps you have a client who's moving and they want to switch plans. Or you might have a client who was enrolled in a Medicare Advantage plan and they want to make the switch to a Medicare Supplement. Regardless of the situation, there may be Guaranteed Issue or Trial right available, allowing them to enroll in a Medigap plan without answering health questions.

Examples of Guaranteed Issue & Trial Rights:

Example: Same Client - Different Situations

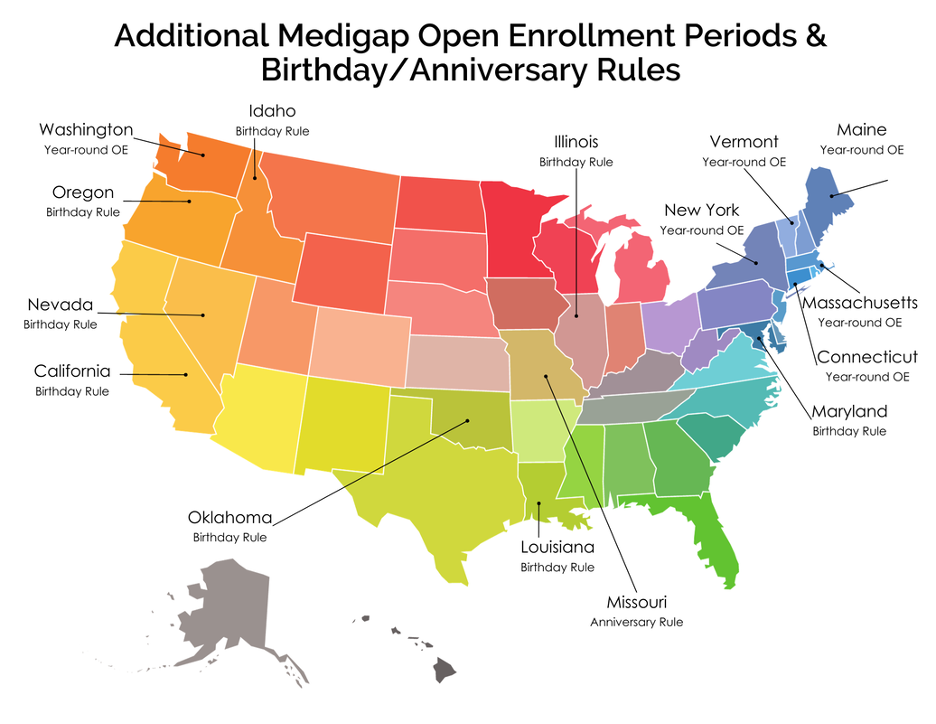

Year-round Enrollment & Other Rules

If your client doesn't fall under any of the Guaranteed Issue/Trial Right situations listed above, there are certain states that have year-round open enrollment periods. There are also states that have birthday and anniversary rules which allow your client to switch plans without going through underwriting. Each state has its own regulations and guidelines so it's important to familiarize yourself with them before enrolling your client in a Medicare Supplement plan.

If your client falls outside of their open enrollment period, doesn't live in a state with year-round open enrollment and doesn't qualify for guaranteed issue rights, they will likely have to go through underwriting; and that requires answering medical and pharmaceutical questions on the application as well as during a phone interview.

If you have any questions regarding Guaranteed Issue rights, birthday rules or getting your client through underwriting, please reach out to us and we'll be happy to assist you. Additionally, feel free to download our Medicare Enrollment Periods guide.

Being an independent insurance agent is a rewarding career, but the challenges that can come with marketing yourself and rising above the competition can be daunting. There are some clear and actionable strategies you can put into place to attract more clients and market yourself effectively.

Your Audience When you think about the insurance products you offer, think about the target audience you want to focus on. If you only sell senior healthcare products, you want to make sure your message is targeting the senior demographic. If you sell Life insurance and Annuities, you have a much broader demographic that you can target. The goal is to reach your target audience with content that is meaningful to them. Your Website People research everything online and that most definitely includes insurance products. If they stumble upon your website and you have little to no valuable information to share with them, they will quickly move on. Make sure your website is up to date, has a clear call to action, has your contact information easily accessible, offers the ability to run quotes, has informative information that educates the visitor about the products you offer and be sure your website is mobile-friendly. These are hard, fast rules that you need to have implemented. If your website isn't current and leaves the visitor feeling that you're not an expert in your field, they will not do business with you. You have one time to make a first impression, and your website is it. SEO (Search Engine Optimization) is a complicated and ever-changing process that search engines continuously tweak. If your website isn't getting much traffic, then it may be time to consider working with a professional. Ranking high in search results takes a lot of work and it's not something that happens overnight.

Meet Them Where They Are

Think about the age of your clients. Baby Boomers who are enrolling in Medicare do more online than you may give them credit for. They bank online, have social media accounts, shop online, research online. Millennials, X-Geners and Gen Z do everything online. I personally, don't remember the last time I picked up a newspaper, listened to the radio, wrote a check, used cash or walked into a bank and I'm Gen X. The point is, people do things very differently today vs. 10 or 20 years ago. It's crucial to pivot and meet people where they are. Advertising Free advertising exists and it's available on your social media accounts. Sharing relevant, educational, informative content vs. the standard, run-of-the-mill content churned out by every other agent is what will set you apart. Paid advertising on social media will get you even further and it won't break your budget. Running ads on Google is a whole other game that is best left to the professionals. It's a complicated bidding process that no amateur should enter into. If you want to run ads on Google, be sure to research a marketing firm that can assist you with that and be prepared to pay for that service. There are many facets to running Google ads and where they will be displayed, as well as many types: search ads, display ads and video ads to name a few. Conclusion Don't let the agent down the street take your clients away from you because you don't have a marketing strategy in place. Be vigilant with your efforts and reach out to us if you need assistance. In this day and age, it's imperative to take the reins and make marketing an integral part of running your business.

After the Medicare Annual Enrollment Period ends on December 7th it's natural to slow down during the last couple weeks of the year after the frenetic pace you've endured since October. And it's important to regroup and plan for the coming year ahead. As part of your New Year's business strategy think about creating a Wellness Strategy for your clients. Sit down, be it virtually or face-to-face, and talk to them about ALL of their insurance needs. After all, they were pummeled with Medicare ads and mailings for months, and that was their (and your) primary focus. Come the New Year though, it's a great time to think about the bigger picture. As you know there are an array of insurance products available on the market that can be hugely beneficial to your clients, but until you talk to them, they may never know about them or even worse...be headed for a catastrophe if they're under-insured.

Let's face it, the last thing anyone wants is to be up-selled, and that's not what this blog post is about. It's about getting to know your clients and learning about their individual needs. We're going to take a dive into some of the insurance products you can discuss with your clients to create a well-rounded solution for 2023. No one wants to be up-selled, but having sufficient coverage is crucial.

To start off, consider discussing Critical Illness insurance which can be so important if a client suffers a heart attack, stroke or a cancer diagnosis. Some plans even cover other illnesses such as Parkinson's Disease, End Stage Renal failure and Multiple Sclerosis, among others. Explain to your clients how Critical Illness insurance works and that a lump sum is paid out to the beneficiary once a diagnosis has been made that can help cover the costs that add up quickly. It's very affordable and creates a safety net in the event they need to access a large sum of money in the future. Relay to them that it can be used for any number of things, including mortgage payments, rent, groceries, child care, etc. It does not have to be used strictly for medical bills.

More than 25% of Americans become disabled before retirement, and on average the disability lasts more than three months, making Disability insurance an important topic to discuss. Go over the fact that there are Short-term and Long-term policies available and they typically cover 60 - 80% of a beneficiary's monthly income. The policy will include details about what constitutes a disability and how the payout will be made. The funds can then be used for bills or day-to-day living expenses. Remind them that premiums can vary depending upon the insurance carrier and their job occupation can also affect rates. Dental, Vision and Hearing insurance is hugely important. Original Medicare Parts A and B do not cover dental, vision or hearing, as they're probably aware. And unfortunately Medicare Supplement policies do not cover these items either. Some Medicare Advantage plans may cover portions of the costs, but it depends upon the plan. Having an affordable DVH plan to help cover the costs of cleanings, fillings, tooth extractions, dentures, eye exams, eyeglasses, contact lenses, hearing exams and hearing aids just makes so much sense. Talk to your clients about getting them on a plan if they don't currently have one in place. Now let's get into long-term care. This is a must-have conversation with your clients as 70% of people over the age of 65 will need some type of long-term care in their lifetime. Explain to them that Medicare does not cover the costs of long-term care and the costs of private nursing home rooms or even semi-private rooms are absolutely staggering. You can share the 2022 costs for long-term care services provided by Mutual of Omaha's '2022 Cost of Care' study below.

Life insurance is for the living. We've all heard that phrase, and if your clients haven't heard it, be sure to use it. Explaining how Life insurance works - that it's not for those who've passed away - it's there to protect and help loved ones during an incredibly difficult time - will help them understand the need for it. You can review the different types of Life insurance available below and review any existing policies they may already have in place.

The New Year is a great time to have conversations with your clients to learn about their health, wealth and lifestyle so you can create the best solution for them. Setting aside time with them after the holiday rush is over and resolutions kick in is ideal. Take the time to reach out to your clients and create a Wellness strategy to set them up for an amazing year ahead. If you need assistance with product selection, have questions about rates or underwriting, simply reach out to us. We're always here to help.

|

Categories

All

|

RSS Feed

RSS Feed