The Resource Blog

|

|

|

Medicare Open Enrollment vs Guaranteed Issue Rights

Medicare Supplements (Medigap policies) have two different types of enrollment periods that don’t require you to answer health (medical) questions. These different periods of time are called a few different names which can be obscure. Here is a break down to better understand the different terms and their specific rules. Medicare Supplement (Medigap) Open Enrollment This period is considered your “initial enrollment period”. Thus the reason it is called your “initial enrollment period” is that many confuse the Medigap Open Enrollment period with the Medicare Open Enrollment period. Medicare Open Enrollment permits someone to change their Medicare Drug or Medicare Advantage plan each year, whereas Medigap’s Open Enrollment normally only allows you ONE guaranteed enrollment period, regardless of preexisting conditions.This period lasts six months and begins the first day of the month in which you are 65 or older and enrolled in Medicare Part B. So if you turn 65 on April 3 but don’t join Medicare B until May 25, your Medigap Open Enrollment Period will start on June 1, which is the first day of the month in which you are both 65 and enrolled in Part B. (Some States such as CA, have a 30 day Medigap Birthday rule that allows you to switch Medigap plans to an equal or lesser value than your current Medigap plan during your birth month-without answering health questions). Medigap Guaranteed Issue Rights The chart below describes the situations, under federal law, that give you a right to buy a policy, the kind of policy you can buy, and when you can or must apply for it. States may provide additional Medigap guaranteed issue rights.

Source: 2017 Choosing A Medigap Policy

Every year from October 15th until December 7th seniors look to make changes to their Medigap coverage. Many rush into a Medicare Advantage plan as they are affordable and often times they get automatically enrolled by their healthcare provider (with written notice). As an advisor, it’s crucial to inform your clients about the differences between Medicare Supplement plans and Medicare Advantage plans. | The name may have “advantage” in it, but is it truly advantageous? Medicare Supplement plans can be very affordable. They don’t have to cost your clients thousands of dollars a year. Many seniors on fixed incomes look to Medicare Advantage plans because they see the difference in pricing. However, these “advantageous” plans change from year to year. One year your client may be covered and have their physicians and hospital of choice in network, and the following year that can all be taken away from them. Medicare Supplement plans can never be changed or altered. Unless your client lapses on policy payments, they will never have to worry about being covered for their healthcare costs. That one, simple fact provides peace of mind for countless seniors. If given the choice to pay slightly more for a plan that will never knock them out of network, why wouldn’t they choose that option? | Medicare Supplement plans offer freedom of choice to select any doctor…anywhere. We believe that Medicare Supplement plans are truly the best coverage for seniors bridging the gap that traditional Medicare doesn’t cover for certain healthcare costs. The plans are stable and the carriers we offer are all A rated. We welcome your questions and concerns, and can sit down with you and explain in detail the pros and cons of Medicare Supplement vs. Medicare Advantage. Allowing you to then inform your client with carefully considered options. | Your clients may only get this one opportunity to make the best choice. Posted by Carolyn Portanova

From October 15th - December 7th, you have the ability to increase your income dramatically. Many agents write 1/3 - 1/2 of their annual Medicare Supplement business in the 4th quarter every year. Do you? Why does this happen? Additional money for the holidays? More likely it is because of the constant Medicare Advantage Annual Election period buzz that begins in September and continues unabated until December. Tens of millions of direct mail pieces, TV, radio and print ads all help stir up the crowds. Agents who write Medicare Supplement can capitalize on all of this free marketing by reaching out to their clients and prospects. This is an opportune time for agents to reassess their current clients' Medicare Supplement plans to be sure they still have the best plan for their needs, AND, to assist prospects with their needs. Medicare Supplement Agent Benefits    Medicare Supplement Client Benefits Medicare Supplement plans can NEVER be cancelled or changed by anyone other than the policy holder, although rates can change annually. Medicare Supplement plans offer the freedom to select any doctor anywhere. The insurance company does not decide which doctors your clients must use. Medicare Supplement plans limit the out-of-pocket expenses incurred by policy holders.

Medicare Advantage plans require policy holders to enroll each year and they receive that year's benefits, providers and cost. Your Role as an Advisor Our Senior Solutions Managers can offer you guidance with which plans are best for your clients' needs. They can assist you with using our quote tool to determine the best plan, depending on your clients' location, health and budget.

Our Senior Solutions Managers    Our Proprietary Quote Tool for Senior Health Coverage To learn more about this FREE tool that provides current information and rates that are updated daily for quotes, NAIC carrier information, carrier-specific medical impairment guides for 90+ different medical conditions, and each carrier's state-specific Medicare Supplement applications, please click below. This tool is available 24/7 with an internet connection, and is complimentary to our contracted agents. However, we do offer a FREE trial access period. By Carolyn Portanova and Sam Corey, Jr.

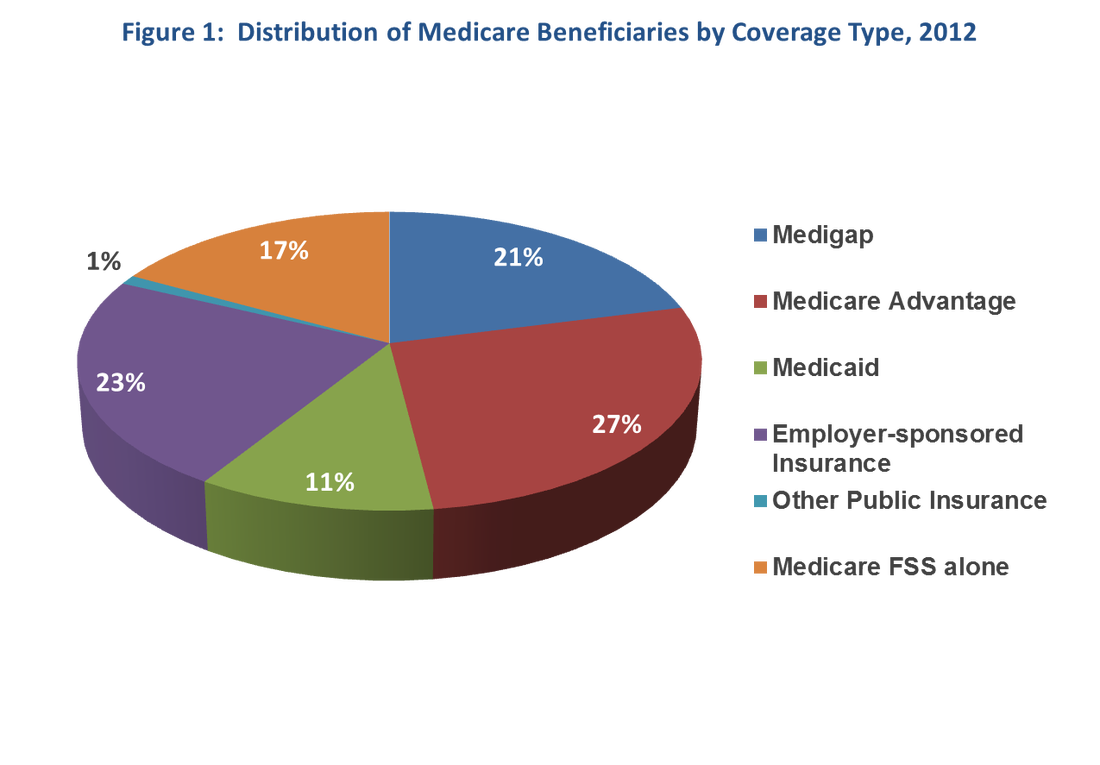

According to the National Association of Insurance Carriers, 58% of Medigap beneficiaries were women in 2012, with 40% of enrollees earning lower than $30,000 per year. To read the full report, click here.   February 14th is the last day for your clients to make the switch from a Medicare Advantage plan and switch back to original Medicare, and purchase a Medicare Supplement plan.

These next few days are crucial if you think you have clients that should make the switch, and can afford a competitively priced Medicare Supplement plan. Plans F and G are the most popular plans and combine one of those with a Part D prescription plan, and your client now has peace of mind. If you have clients that need to make the switch, and are unsure of which plan would make the most sense for them, then please call us. We have the tools and resources to assist you in growing your business, by expanding your product portfolio. By Carolyn Portanova |

Categories

All

|

RSS Feed

RSS Feed